Welcome to Robbyn's real estate blog. An essential online place for information and updates about real estate, community, laws and sometimes just good old fachioned fun topics. Look at this as your first stop to search for informationwhen putting together your plan to buy or sell real estae with Robbyn Battles.

Menu

Close

Main Content

Home

Slideshow

Robbyn'sSignature Property Videos

Video is crucial in today's real estate market. Property videos are an industry minimum standard. Robbyn Battles provides an array of short and long property videos. From "Reels" to digital property brochures, digital media is easily accessible to every potential homebuyer.

Serving your CommunityFor Over 30 Years

“Buying, selling putting all the pieces together. To say I sell real estate is not completely accurate; I’m a facilitator. I help put all the pieces together. I create a plan with the end result being the sale of real estate. My job is to listen to your concerns, wants, and needs, facilitate the process, and help you feel comfortable and confident that I can sell your home. Then together, we have a successful transaction. Let's plan your next move."

Let's Get StartedHow Can I Help

Robbyn Battles has been in the real estate business for more than 30 years, and for her, "The business just gets better and better!" Born to parents who are both real estate professionals, Robbyn grew up in the industry. Spending much of her childhood in their office, at 13 years old, she was already assisting agents in their company. When her parents transitioned to building custom homes, she took the reins of their real estate business, and the rest is history..

Robbyn is a Certified Senior Specialist and a Certified Luxury Home Marketing Specialist. She's also ranked among the Top 1% of Agents in the US in 2022 by RealTrends. Another item on her long list of accomplishments, she was appointed by the LA County Supervisor's Office as a Commissioner on the LA County Tax Appeals Board. Read her entire Bio on her About page.

News from Robbyn

April 25, 2024April Monthly Letter

Dear Reader, Welcome to my April monthly letter. This month has been bustling with activity! I spent the initial weeks assisting a client...

Learn More

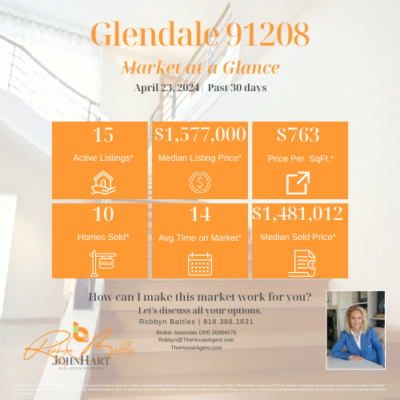

April 24, 2024Glendale 91208 April Market at a Glance

Glendale 91208 April Market at a Glance. Keeping abreast of the latest market activity is crucial for anyone inv...

Learn More

April 23, 2024Discover Pasadena and the Arts

A love for fine art and football may seem dissimilar passions, but both can be satisfied in a city 10 miles from downtown Los Angeles. Pa...

Learn More